Published Jul 04, 2026 • Market Analysis

Automated Trading Strategy Testing Solutions: Building Robust Strategies Beyond Backguessing

The landscape of modern finance is increasingly dominated by algorithms. Once the exclusive domain of institutional players, algorithmic trading now accounts for a staggering 70% of futures volume, a figure that underscores the necessity of systematic approaches for traders at all levels. Yet, simply deploying a strategy without rigorous, automated testing is akin to "backguessing" — a high-stakes gamble in a sophisticated market. True automated trading demands solutions that go beyond basic historical simulations, offering institutional-grade validation to ensure robustness and profitability.

Key Takeaways

Algorithmic trading comprises approximately 70% of futures market volume, signaling a shift towards systematic trading that necessitates robust testing.

Traditional "backtesting" with one-minute data often leaves 98% of the trading day unanalyzed, highlighting the critical need for tick-level precision in modern testing solutions.

Effective strategy validation extends beyond in-sample performance, requiring comprehensive out-of-sample testing, Monte Carlo simulations, and parameter sensitivity analysis to mitigate overfitting.

Institutional-grade testing platforms provide crucial features like multi-asset support, detailed performance metrics (e.g., Sharpe ratio, maximum drawdown), and optimization heatmaps to identify stable strategy parameters.

Automated trading strategy testing should simulate real-world execution costs—such as spread, commission, and slippage—and provide seamless integration for paper and live trading to ensure fidelity from development to deployment.

The Imperative of Backtesting in Automated Trading

Automated trading strategies, unlike discretionary approaches, execute predefined rules mechanically. This mechanical execution offers discipline and speed but also introduces a critical dependency: the inherent soundness of those rules. If a strategy's logic contains flaws, automation will consistently replicate those flaws, leading to consistent losses in a live environment. Backtesting, therefore, serves as the indispensable quality control for any automated system, identifying whether a strategy possesses a positive expectancy across diverse market environments before real capital is deployed ClearEdge Trading.

Research from the Futures Industry Association highlights the dramatic rise of algorithmic trading, which now constitutes roughly 70% of futures volume. This dominance by algorithms isn't accidental; institutional traders, with their substantial capital requirements, rely heavily on extensive backtesting for statistical validation. This rigorous discipline, once confined to quantitative hedge funds, is now accessible and crucial for retail traders aiming for professional-level operation.

The primary goal of backtesting is to validate the strategy's core logic and its technical implementation. Questions such as "Does the stop-loss logic work as intended?", "Are position sizes appropriate for account capital?", or "Do entry conditions trigger too frequently or rarely?" are all systematically answered through this process. A strategy might perform well during trending markets but fail catastrophically during consolidation, or prove effective on one asset class but poorly on another. Backtesting across multiple conditions reveals these limitations, preventing costly mistakes in live trading ClearEdge Trading.

Actionable Takeaway: Prioritize backtesting as the foundational step for any automated strategy. Ensure your chosen testing solution can simulate diverse market conditions and thoroughly validate both strategy logic and technical implementation to uncover potential flaws before they impact real capital.

Beyond Simple Simulations: Features of Institutional-Grade Testing Platforms

While basic backtesting might involve running a strategy against historical daily data, professional-grade automated trading demands a far more sophisticated approach. The goal is not just to see if a strategy made money in the past, but to understand *why* it did, and if that performance is likely to persist in the future. This requires advanced features that address data integrity, execution fidelity, and statistical robustness.

One critical area is data resolution. Many retail backtesting solutions still rely on one-minute quotes, a level of granularity that significantly compromises accuracy. As one platform accurately observes, "One-minute quotes leave 98% of the trading day without data," effectively turning backtesting into "backguessing" tradeSteward. Institutional-grade platforms offer tick-level precision, often down to 1-second resolution or finer, ensuring that simulations reflect actual market movements, including intra-bar fluctuations, with greater accuracy. This detailed data is vital for high-frequency or even basic intraday strategies where price action within a minute can be significant QuantStart.

Furthermore, an effective testing solution must provide:

Comprehensive Performance Metrics: Beyond raw profit, metrics like Sharpe ratio, Sortino ratio, maximum drawdown, Calmar ratio, and win rate are essential for a holistic understanding of risk-adjusted returns. Detailed reports, including equity curves and trade statistics, provide clear visual and quantitative insights into strategy performance Goat Funded Trader.

Realistic Execution Simulation: The ability to account for real-world costs such as spread, commission, and slippage during backtesting is paramount. Without this, a strategy that appears profitable on paper might become unprofitable in live trading. Some platforms even simulate order types (market, limit, stop) and automatic position sizing with precision, mirroring live trade execution TradeZella.

Multi-Asset Support: Professional traders often diversify across various asset classes. A robust testing solution should support multiple assets—stocks, forex, cryptocurrencies, futures, and options—allowing traders to validate their strategies across their entire portfolio TradeZella.

Actionable Takeaway: When evaluating automated strategy testing solutions, prioritize platforms that offer tick-level data resolution, comprehensive risk-adjusted performance metrics, and realistic execution cost simulations across all relevant asset classes to ensure your backtest results accurately reflect potential live performance.

Mitigating Bias: Out-of-Sample Testing and Robustness Checks

One of the most insidious dangers in automated strategy development is overfitting, where a strategy performs exceptionally well on historical data (in-sample) but fails miserably in real-time trading (out-of-sample). This typically occurs when a strategy's parameters are overly optimized to past market noise rather than capturing a genuine, persistent edge. Institutional-grade platforms employ sophisticated techniques to combat this bias and ensure true robustness.

Out-of-Sample Testing: A fundamental practice, this involves holding back a portion of historical data (e.g., the most recent 20-30%) that the strategy has never "seen" during its development or initial optimization. After optimizing parameters on the "in-sample" data, the strategy is then run on the "out-of-sample" segment. If performance significantly deteriorates, it's a strong indicator of overfitting. The ability to perform this naturally and easily within a testing environment is crucial for professional traders QuantStart.

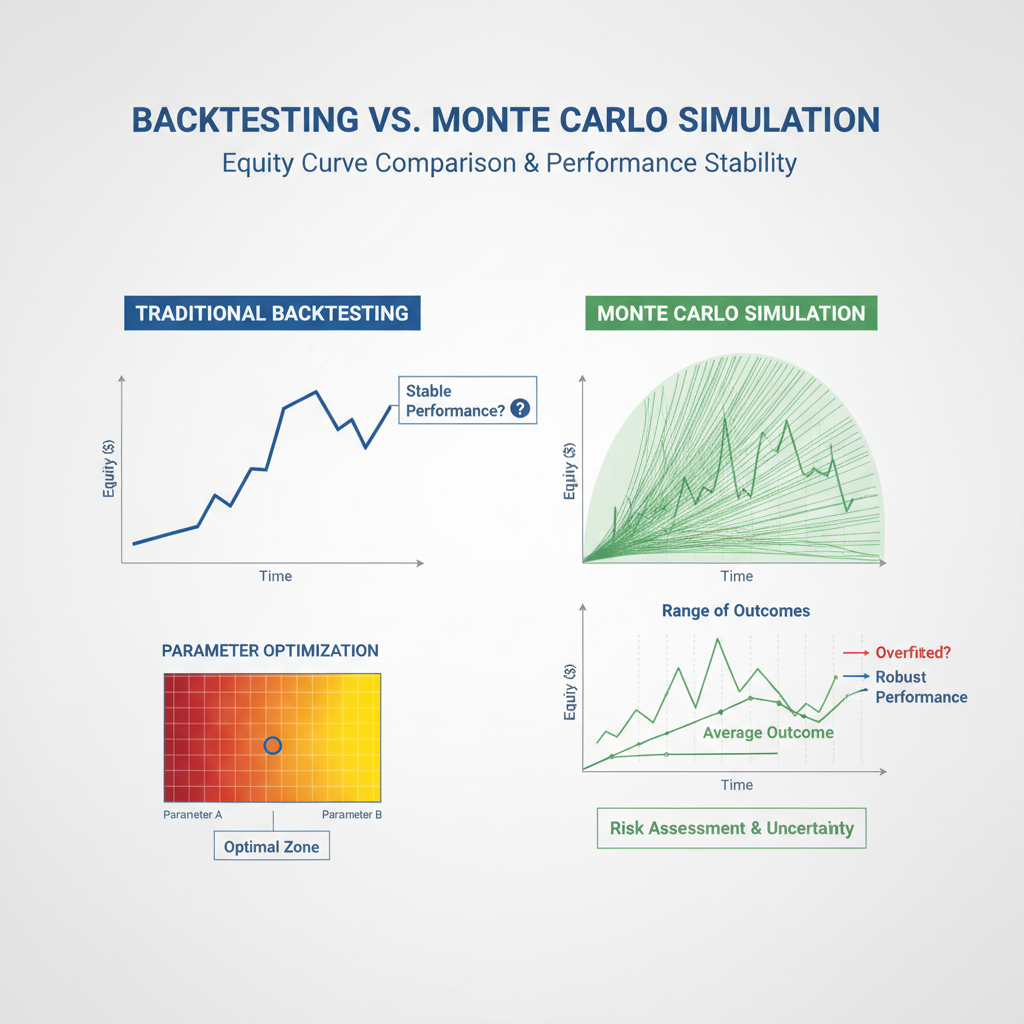

Parameter Optimization and Sensitivity Analysis: Strategies often rely on various parameters (e.g., moving average periods, RSI thresholds). Manually testing every combination is impractical. Advanced platforms offer optimization features that can run thousands of full backtests with varying parameter sets, completing weeks of work in minutes QuantConnect. Crucially, these systems visualize the results on heatmaps, which allow traders to quickly understand a strategy's sensitivity to specific parameters. A robust strategy will show stable performance across a wider range of parameter values, rather than spiking only for a very narrow, specific set. For instance, if a strategy only performs well with an RSI period of exactly 14, but dramatically fails at 13 or 15, it suggests extreme sensitivity and potential overfitting.

Monte Carlo Simulation: This advanced technique addresses the uncertainty inherent in sequential trade outcomes. Instead of simply replaying historical trades, Monte Carlo simulations randomly reorder the historical trades or introduce slight variations to entry/exit points and P&L. By running thousands of such randomized simulations, it generates a distribution of possible equity curves, revealing the probabilistic robustness of a strategy under varied (but realistic) sequences of wins and losses. This helps gauge the likelihood of different outcomes and provides a more realistic assessment of risk and potential performance QuantStart.

Actionable Takeaway: Always prioritize testing methodologies that actively combat overfitting. Utilize out-of-sample data validation, leverage parameter optimization with heatmap visualization for sensitivity analysis, and incorporate Monte Carlo simulations to understand the probabilistic robustness of your strategy against market randomness.

The Technical Architecture: Data Integration and System Reliability

The efficacy of any automated trading strategy testing solution is intrinsically linked to its underlying technical architecture. This encompasses everything from the quality and breadth of available data to the sophistication of the testing engine and its ability to integrate with live trading environments.

Data Management and Access: High-quality historical data is the bedrock of reliable backtesting. This includes not just price data but also order flow data, volume, and potentially alternative datasets. Platforms that allow for custom data sources, such as CSV imports, offer greater flexibility for traders working with unique datasets Goat Funded Trader. Decades of historical data are often required for long-term studies, enabling traders to validate strategies across various economic cycles and market regimes Goat Funded Trader. The ability to access multi-timeframe analysis is also crucial for strategies that rely on different scales of market movement.

Seamless Transition to Live Trading: A primary benefit of integrated testing platforms is the smooth transition from backtesting to live automated trading. These systems often provide an all-in-one solution for data collection, strategy development, historical backtesting, and live execution, eliminating the need to move strategies between disparate systems. This integration minimizes errors and ensures that the live environment closely mimics the tested environment, critical for maintaining the integrity of an automated system QuantStart.

Broker Integration and Execution Fidelity: For automated execution, robust broker integration is essential. Many platforms, like cTrader and MetaTrader 5, are popular among forex and CFD traders precisely because they integrate strategy testing directly with broker services. This provides a clean environment for evaluating bots on historical data and offers a clear path to live automated trading. The platform should simulate broker commissions, slippage, and real-time data feeds accurately. For larger capital bases, optimized execution algorithms that attempt to minimize transaction costs become particularly useful QuantStart.

Advanced Considerations for Latency: While often beyond the scope of most retail traders, institutional players frequently consider factors like exchange co-location for latency minimization. This involves placing dedicated servers directly at the exchange data center, a prohibitively expensive option for nearly all retail algorithmic traders unless very well capitalized. However, for those operating at a professional level, understanding the impact of latency on high-frequency strategies is crucial, and the choice of platform can influence how effectively these concerns are addressed, perhaps through proximity to exchange data centers via VPS systems QuantStart.

Actionable Takeaway: When selecting an automated trading strategy testing solution, evaluate its data management capabilities, ensuring high-quality, tick-level data and flexibility for custom inputs. Prioritize platforms offering seamless integration from backtesting to automated live execution, alongside robust broker connectivity that accurately simulates real-world trading costs.

How Horizon Addresses This

Horizon offers an integrated, institutional-grade AI trading platform designed specifically for serious traders who require sophisticated testing solutions without the need for complex coding. Recognizing the pain points of inadequate backtesting and the desire for robust strategy validation, Horizon empowers users to transform their trading ideas into automated, disciplined execution.

Our platform directly addresses the challenges outlined above by providing an institutional-grade backtesting engine. This engine doesn't just run historical simulations; it offers detailed performance metrics including Sharpe ratio, Sortino ratio, max drawdown, and out-of-sample backtesting capabilities to rigorously validate your edge. To combat overfitting and ensure robustness, Horizon integrates Monte Carlo simulations and visual heatmaps for parameter sensitivity analysis, allowing traders to identify stable and reliable strategy configurations. This ensures that your strategies are not merely backguessed, but thoroughly tested against various market conditions and potential future scenarios.

Furthermore, Horizon supports multi-asset trading (stocks, forex, crypto, futures, options) and provides tick-level data resolution for unparalleled accuracy in simulations. With AI-powered strategy generation, traders can rapidly iterate and test custom strategies without writing a single line of code. Once validated, strategies can be deployed for live trading via robust broker integrations, ensuring a smooth transition from research to automated execution. For those looking to learn or expand, our marketplace offers community-built strategies, allowing users to buy, copy, or sell access to proven approaches with transparent performance records.

Horizon provides the professional trader with a comprehensive ecosystem for developing, testing, and deploying automated strategies, bridging the gap between sophisticated quantitative finance and accessible, intuitive technology. Explore Horizon's powerful capabilities to elevate your automated trading to the next level today.

Conclusion

The journey from a promising trading idea to a consistently profitable automated strategy is paved with rigorous testing. As algorithmic trading continues to dominate global markets, the demand for sophisticated, institutional-grade testing solutions has never been higher. Moving beyond simplistic historical replays to embrace tick-level precision, out-of-sample validation, Monte Carlo simulations, and comprehensive robustness checks is no longer an advantage, but a necessity for serious traders. These advanced capabilities ensure that strategies are not merely optimized for past data but are genuinely robust and adaptable to future market dynamics. By leveraging platforms that offer such a comprehensive testing environment, traders can significantly de-risk their automated systems and operate with the confidence required to succeed in today's complex financial landscape. Embrace the power of systematic validation to transform your trading edge into automated, disciplined execution at horizon.trade