Published Jul 04, 2026 • AI Insights

Automated Trading Strategy Testing Tools Explained: A Professional's Guide

In an era where algorithmic strategies execute the majority of market volume, the distinction between a speculative idea and a statistically robust trading edge hinges on sophisticated, automated testing. The notion that gut instinct or manual analysis alone can consistently outperform a disciplined, data-driven approach is increasingly a relic of the past. As much as most trading volume is now executed by automated algorithms, as noted by Forex Tester Online, the imperative for serious traders to master automated strategy testing has never been greater.

Key Takeaways

Automated algorithms now execute the majority of market volume, underscoring the necessity for systematic strategy development and rigorous testing to maintain a competitive edge.

Effective automated testing extends beyond basic backtesting to include advanced validation techniques like out-of-sample backtesting, Monte Carlo simulations, and walk-forward analysis, crucial for mitigating overfitting and ensuring real-world robustness.

Specialized platforms offer diverse features for automated testing, from tick-level precision and multi-threaded optimization (MetaTrader 5, cTrader) to natural language strategy setup and AI-generated models (TradeStation), catering to varying levels of technical proficiency.

Walk-forward testing is a critical method to validate strategy robustness, identifying whether a strategy maintains efficacy across different market conditions by exposing it to unseen data, thereby mitigating overfitting, as explained by Paperswithbacktest.com.

For traders without coding expertise, modern AI-powered platforms are democratizing access to institutional-grade testing, enabling the generation, backtesting, and deployment of complex strategies with no coding required.

The Imperative of Automated Testing in Modern Markets

The financial markets have undergone a profound transformation, shifting from floor-based trading to highly automated, electronic systems. This evolution demands a strategic response from traders. "Algorithmic trading stands apart from other types of investment classes because we can more reliably provide expectations about future performance from past performance, as a consequence of abundant data availability," states QuantStart. This availability of data, coupled with advancements in computational power, makes automated strategy testing not merely an advantage but a fundamental requirement for success.

The speed and scale at which modern markets operate mean human traders are often outmatched by algorithms. Automated testing allows for the rapid evaluation of thousands of potential strategies, identifying those with a statistical edge far beyond what manual analysis could achieve.

The discipline inherent in automated testing also removes emotional biases, a notorious pitfall for discretionary traders. By codifying a strategy's rules and backtesting them rigorously, traders can obtain objective insights into potential profitability, risk exposure, and overall strategy robustness. This systematic approach is crucial for managing capital effectively and preparing for the psychological challenges inherent in trading, especially during periods of drawdown where "many strategies that have been shown to be highly profitable in a backtest can be ruined by simple interference," as highlighted by QuantStart. Without automated testing, even a well-conceived idea remains an unverified hypothesis, prone to failure in live markets.

Actionable Takeaway: Embrace automated testing as the foundational step for any trading strategy. It ensures objectivity, scalability, and emotional detachment, providing a clearer path to validating and refining your market edge.

Core Principles of Robust Strategy Testing

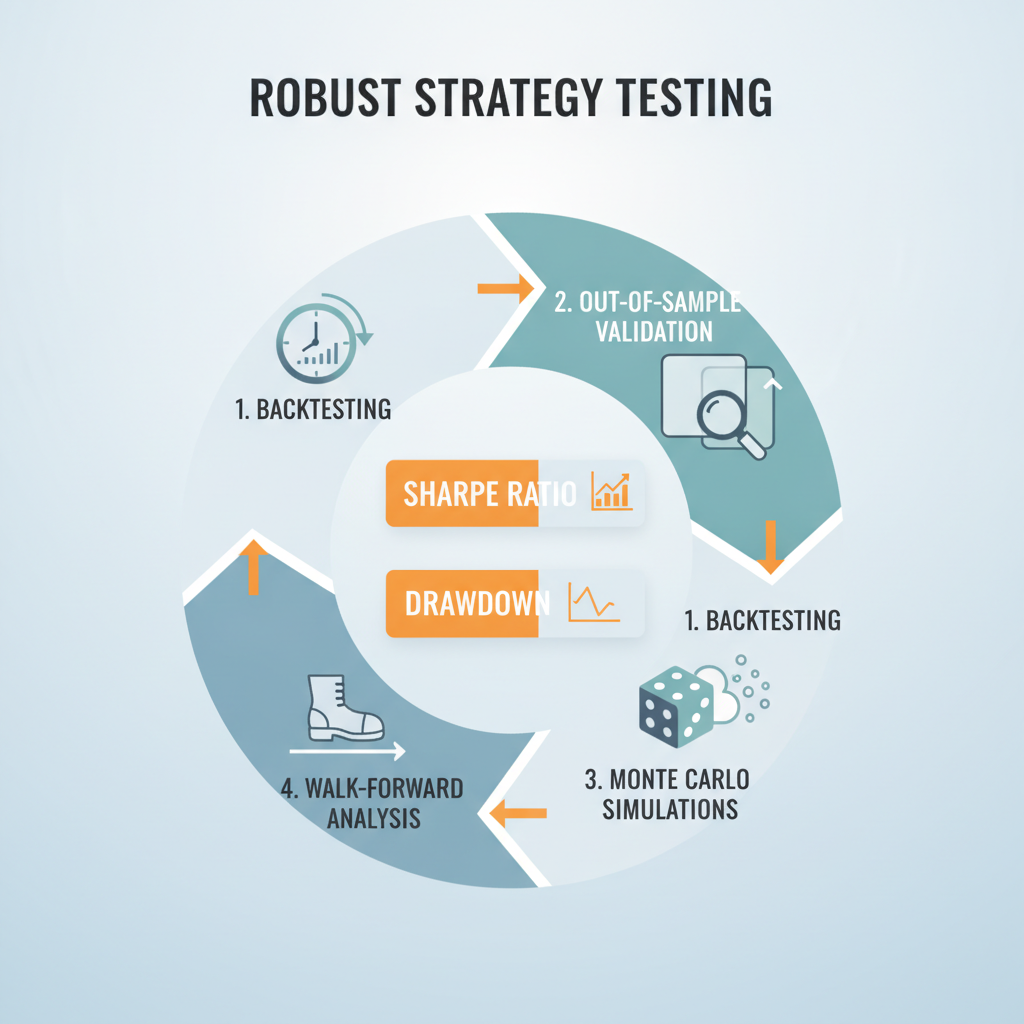

At its heart, automated strategy testing involves simulating a trading strategy against historical market data. This process, known as backtesting, evaluates how a strategy would have performed in the past, generating key metrics such as total return, Sharpe ratio, maximum drawdown, and profit factor. However, robust testing goes far beyond a simple backtest.

Understanding Backtesting and Its Limitations

A basic backtest provides a preliminary snapshot of performance. For instance, platforms like MetaTrader 4 (MT4) offer a "Strategy Tester" tool to evaluate Expert Advisors (EAs), providing data on "profit-loss percentage ratio, the amount of profitable and loss-making trades in a given period, the risk factors involved and more," according to IG. Similarly, MetaTrader 5 (MT5) includes a "built-in tester for automated strategy simulations" with access to "extensive historical forex and CFD data," and "multi-threaded optimization for faster results," as noted in a review by Goat Funded Trader.

However, a key limitation is overfitting—where a strategy performs exceptionally well on the historical data it was optimized on but fails in live trading. This is where advanced testing methodologies become critical.

Advanced Validation Techniques for True Robustness

Out-of-Sample Backtesting: This involves splitting historical data into two segments: an "in-sample" period for strategy development and optimization, and an "out-of-sample" period for testing the strategy on unseen data. A strategy's performance on out-of-sample data is a much stronger indicator of its potential future viability.

Monte Carlo Simulations: Instead of a single historical run, Monte Carlo simulations generate hundreds or thousands of hypothetical market scenarios based on historical volatility and price movements. By running the strategy through these diverse scenarios, traders can assess the range of possible outcomes and understand the strategy's sensitivity to market randomness and tail risks.

Walk-Forward Analysis: "Walk forward testing offers insights into the robustness of a trading system," as detailed by Paperswithbacktest.com. This iterative process involves optimizing a strategy on an initial segment of historical data, then testing it on a subsequent, unseen segment. This "walk-forward" window is then shifted, and the process is repeated. This "iterative nature... contributes to an adaptive optimization process," helping to refine parameters and adapt to evolving market conditions.

Heatmaps and Sensitivity Analysis: These tools visualize how a strategy's performance changes across different parameter values. By mapping profitability or risk metrics, traders can identify robust parameter ranges that are less sensitive to minor adjustments, rather than relying on a single "optimal" set of parameters that might be overly specific to past data.

Actionable Takeaway: Do not rely solely on in-sample backtesting. Always incorporate out-of-sample data, consider Monte Carlo simulations for probabilistic outcomes, and prioritize walk-forward analysis to ensure your strategy's adaptability and robustness across varying market conditions.

Navigating the Automated Trading Strategy Testing Tool Landscape

The market offers a wide array of tools for automated strategy testing, ranging from broker-integrated platforms to standalone software and code-based environments. The "right" tool depends on a trader's technical expertise, asset classes of interest, and desired level of customization.

Broker-Integrated Platforms: Convenience and Execution

Many popular trading platforms, particularly in forex and CFD markets, integrate backtesting capabilities directly. These often provide seamless transitions from testing to live automated execution.

MetaTrader 4/5: Widely adopted, MetaTrader platforms offer a "Strategy Tester" for their Expert Advisors (EAs). MT5, for example, boasts "built-in tester for automated strategy simulations," "access to extensive historical forex and CFD data," and "multi-threaded optimization for faster results," according to Goat Funded Trader. While powerful for its user base, developing custom strategies often requires proficiency in their proprietary MQL4/MQL5 languages.

cTrader: "Popular among forex and CFD traders," cTrader includes "built-in tools for automated strategy testing with strong broker integration." Key features include "support for backtesting on Renko and range bar charts," "visual mode for interactive step-by-step simulation," and "tick-level precision with spread and commission adjustments." This makes it appealing for traders focused on detailed market microstructure analysis, as described by Goat Funded Trader.

Advanced & Multi-Asset Platforms: Depth and Customization

For traders seeking more advanced capabilities or multi-asset support, dedicated platforms offer greater depth in backtesting and customization.

NinjaTrader: "Tailored for futures trading," NinjaTrader provides "robust historical simulations and direct market access." It's known for its precision in execution modeling and advanced analytics, making it a staple for futures professionals, as per Goat Funded Trader.

TradeStation: Offering a more comprehensive suite, TradeStation includes features like "automated recognition of chart patterns and candlesticks," "natural language inputs for strategy setup," and "AI-generated models for machine learning-based testing." This caters to a broader range of traders, including those interested in integrating AI without deep coding knowledge, according to Goat Funded Trader.

Code-Based Environments: Ultimate Control (and Complexity)

For quantitative researchers and developers, programming languages like Python or R, combined with libraries like Pandas and Backtrader, offer the highest degree of control. "Programming skill is an important factor in creating an automated algorithmic trading strategy," notes QuantStart. These environments allow for custom backtesting engines, integration with any data source, and sophisticated algorithm development. "Tools such as Python offer extensive libraries like Pandas and Backtrader that facilitate the development of such testing frameworks," especially for "walk forward testing," as Paperswithbacktest.com illustrates. However, this path demands significant time and expertise in coding and financial modeling.

While powerful, research environments like MATLAB and Pandas, though offering "vectorisation capabilities that allow fast execution speed," are "generally not suitable for strategies that approach intraday trading at higher frequencies on sub-minute scale" or for robustly connecting to real-time market data and brokerage APIs, as detailed by QuantStart.

Actionable Takeaway: Assess your technical skills and specific trading needs. If you're a non-coder, seek platforms with intuitive interfaces or AI-powered generation. If you demand ultimate control and precision, be prepared for the learning curve of code-based solutions.

Beyond Basic Backtesting: Ensuring Real-World Performance

A successful backtest is only the first step. The true challenge lies in bridging the gap between historical simulation and live market performance. Several critical factors and practices must be considered.

Addressing Market Realities: Data Quality, Slippage, and Commissions

The accuracy of your backtest is profoundly influenced by the quality of your historical data. Ideal data includes tick-level granularity, accurate bid-ask spreads, and precise historical transaction costs. Many retail-focused platforms may use interpolated or lower-resolution data, leading to unrealistic backtest results.

Slippage: The difference between the expected price of a trade and the price at which it's executed. Slippage, especially in fast-moving or illiquid markets, can significantly erode strategy profits. Robust backtesting tools should allow for the modeling of realistic slippage.

Commissions and Fees: Every trade incurs costs. Accurately modeling commissions, exchange fees, and financing costs (e.g., overnight fees for leverage) is essential. Small fees can accumulate and turn a theoretically profitable strategy into a losing one in live trading.

Survival Bias: Historical data often only includes currently traded assets, omitting those that failed or were delisted. This can lead to an optimistic bias in backtesting results if not accounted for.

The Role of Walk-Forward Optimization

As discussed, walk-forward testing is a superior method to combat overfitting and ensure a strategy's adaptability. It simulates the real-world process of periodically re-optimizing a strategy to adapt to new market regimes without "peeking" at future data. This "iterative nature of walk forward testing contributes to an adaptive optimization process," allowing for "continuous adaptation to evolving market conditions," as stated by Paperswithbacktest.com. This approach is paramount for maintaining strategy relevance in dynamic markets.

Paper Trading: The Bridge to Live Execution

Before committing real capital, paper trading (or simulation trading) provides a crucial intermediate step. It allows traders to run their automated strategies in real-time market conditions using simulated money. This environment tests the strategy's logic, execution integrity, and the trader's emotional discipline under live market pressures without financial risk. "Real-time execution capabilities post-testing" are often offered by platforms like MetaTrader 5, enabling this transition, notes Goat Funded Trader.

Actionable Takeaway: Demand high-quality data and actively model real-world costs like slippage and commissions in your backtests. Implement walk-forward optimization to ensure adaptability, and always use paper trading as a final validation step before live deployment.

How Horizon Addresses This

Horizon Trade is specifically engineered to empower serious traders who think systematically but may lack coding expertise, addressing the complexities and limitations inherent in traditional automated strategy testing.

Horizon’s platform tackles the challenge of strategy creation with its AI strategy generation feature, allowing users to develop complex trading rules without writing a single line of code. This democratizes access to advanced algorithmic trading, transforming your market insights into deployable strategies.

When it comes to testing, Horizon provides an institutional-grade backtesting engine. This isn't just basic historical simulation; it includes advanced features like out-of-sample backtesting to validate against unseen data, Monte Carlo simulations for probabilistic risk assessment, and heatmaps for robust parameter optimization. These tools are crucial for identifying genuine market edges and mitigating overfitting, ensuring your strategy is truly robust rather than merely lucky on past data. Horizon's backtesting supports multi-asset strategies across stocks, forex, crypto, futures, and options, giving you a comprehensive view.

For ensuring real-world performance, Horizon integrates directly with brokers for automated execution, allowing a smooth transition from a proven backtest to live trading. You can monitor strategy performance with real-time analytics, keeping a pulse on how your algorithms are performing in dynamic market conditions. Furthermore, for those looking to explore proven ideas, Horizon offers a marketplace of community-built strategies, where you can buy, copy, and customize strategies that have verifiable track records, or even sell access to your own strategies, building your reputation on real performance.

Conclusion

The landscape of modern trading is irrevocably shaped by automation. For professional traders, mastering automated strategy testing is no longer a niche skill but a core competency essential for competitive advantage and disciplined capital management. By moving beyond rudimentary backtesting to embrace advanced techniques like out-of-sample validation, Monte Carlo simulations, and walk-forward analysis, traders can build strategies that are genuinely robust and adaptable to ever-changing market conditions. While the complexity of coding has historically been a barrier, innovative platforms are now making institutional-grade tools accessible to a broader audience, bridging the gap between systematic thinking and automated execution. Embrace these advancements to transform your trading edge into a consistently profitable, disciplined, and scalable operation. Explore how horizon.trade can empower your journey into automated strategy development and rigorous testing. For more insights into algorithmic trading, feel free to explore our blog and resources.

Sources

13 Best Software for Backtesting Trading Strategies - Goat Funded Trader

What is Backtesting? How to Backtest a Trading Strategy - IG

Algorithmic trading strategies: A Practical Guide - Finzer.io

Choosing a Platform for Backtesting and Automated Execution - QuantStart

Algorithmic Trading Strategies: Build, Backtest, and Optimize | FTO - Forex Tester Online

Trading Strategy Optimization Explained (Algo Trading) - Paperswithbacktest.com

Successful Backtesting of Algorithmic Trading Strategies - Part I - QuantStart