Published Jun 23, 2026 • Market Analysis

Risk Management: Essential Strategies for Algorithmic Trading

In a landscape where algorithmic strategies now account for a significant portion of daily trading volume – with some estimates placing automated trades as high as 60-73% of US equity volume, up from 20% in 2005 for institutional investors — the margin for error has shrunk dramatically. Without a robust, systematic approach to risk, even the most promising trading ideas can lead to catastrophic losses. This reality elevates risk management from a mere compliance checkbox to a strategic imperative for every serious trader.

Key Takeaways

- Risk management, a formal science since the 1950s, is a systematic process of identifying, assessing, and mitigating threats, distinct from reactive risk assessment.

- Proactive risk identification and comprehensive analysis, including likelihood and severity mapping, are fundamental to constructing resilient trading strategies.

- Effective risk management strategies for algorithmic trading leverage quantitative methods like robust backtesting, Monte Carlo simulations, and stress testing to understand potential downside exposure and validate strategy robustness.

- Risk management is an ongoing, adaptive process that requires continuous monitoring of strategy performance and market conditions, rather than a one-time setup.

- Platforms like Horizon offer institutional-grade tools for AI-powered strategy generation, advanced backtesting, and automated execution with integrated risk controls, enabling traders to systematically manage risk without coding.

Risk management, as defined by the International Organization for Standardization (ISO) in ISO Guide 31073:2022, is the "coordinated activities to direct and control an organization with regard to risk." While its formal scientific study began in the 1950s, with initial research predominantly focused on finance and insurance, its application in modern financial markets has become increasingly sophisticated and critical. For traders operating in an automated environment, the principles of risk management offer a blueprint for disciplined, sustainable success.

Understanding the Core Principles of Risk Management

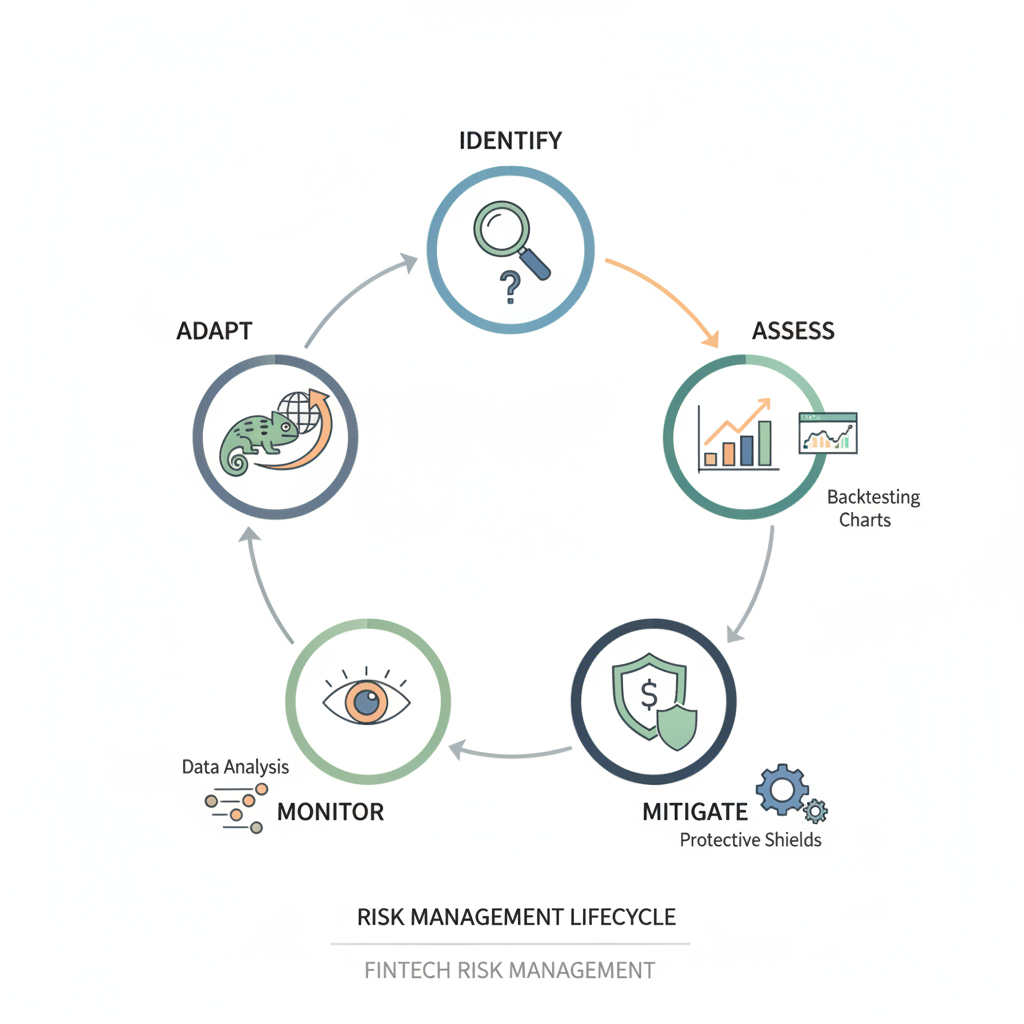

At its core, risk management is a systematic process of identifying, assessing, and addressing potential threats or uncertainties that could impact the achievement of objectives. This systematic approach is crucial because, as the US EPA highlights, it's a distinct process from risk assessment. Risk assessment establishes if a risk is present and its magnitude, while risk management integrates these findings with other considerations (like economic or legal factors) to decide *how* to manage risks effectively.

"Risk management is the systematic process of identifying, assessing, and mitigating threats or uncertainties that can affect your organization." – Harvard Business School Online

The foundational step involves comprehensive risk identification. This isn't just about identifying obvious market risks like volatility or price drops, but also operational risks (e.g., platform outages, data errors) and strategic risks specific to a trading approach. Once identified, risks must be rigorously analyzed to understand their nature, likelihood, and potential severity. Vector Solutions emphasizes mapping likelihood and severity, often using a risk matrix, to prioritize and allocate resources effectively. Without this detailed analysis, risk responses are often reactive and inefficient, leaving traders vulnerable to unforeseen market events.

A practical insight for traders is to categorize risks into broad buckets: market risk (volatility, price gaps), liquidity risk (inability to enter/exit positions), operational risk (system errors, connectivity issues), and model risk (strategy underperformance, overfitting). By clearly defining and documenting potential risks, traders can move from a vague sense of worry to a structured plan of action. This proactive stance, leveraging data analysis to anticipate threats, is what SentinelOne identifies as key to preventing severe financial losses and improving ROI.

Implementing Robust Risk Management Strategies in Algorithmic Trading

The move towards algorithmic trading, driven by the desire for precision and speed, inherently requires more sophisticated and automated risk management protocols. Manual oversight simply cannot keep pace with the execution speed of modern markets. Therefore, embedding risk controls directly into the algorithmic strategy design is not just advantageous but essential.

One of the primary strategies involves position sizing and diversification. Instead of betting a large percentage of capital on a single trade, algorithms can be programmed to automatically scale positions based on a predefined risk tolerance. For instance, a strategy might limit exposure to no more than 2% of total capital per trade, or ensure no single asset class exceeds 20% of the portfolio's value. This kind of systematic approach to allocation mitigates concentration risk, a common pitfall for many traders.

Stop-loss and take-profit orders are classic risk management tools, but in an algorithmic context, they become significantly more powerful. Automated systems can execute these orders instantaneously, preventing emotional decisions or delayed reactions during rapid market movements. Advanced algorithmic strategies can employ dynamic stop-losses that adjust based on market volatility or technical indicators, offering adaptive protection against downside risks. According to DNV, "a risk management strategy is more than a compliance necessity and should be seen as a strategic asset," enabling proactive dealing with threats and seizing opportunities.

Furthermore, implementing circuit breakers or kill switches within an algorithmic framework is a critical layer of protection. These are predefined conditions that, when met, automatically pause or halt all trading activity for a given strategy or even across an entire portfolio. Examples include a predefined maximum daily loss threshold (e.g., -5% of daily capital), excessive drawdown beyond a historical maximum, or significant slippage during execution. Such automated safeguards can prevent runaway losses during extreme market dislocations, reinforcing the point made by IBM that risk management helps protect against "financial expenses, inefficiencies, and reputational damage."

Quantitative Approaches to Risk Management and Portfolio Protection

For serious traders, moving beyond basic risk mitigation involves embracing quantitative methods to truly understand the exposure of their strategies. This is where institutional-grade analysis comes into play, providing deep insights into potential downside scenarios and strategy robustness. These methods transform risk from an abstract concept into measurable, actionable data points.

Backtesting is the cornerstone of quantitative risk management. By simulating a strategy's performance against extensive historical market data, traders can identify how it would have performed under various past market conditions, including periods of high volatility or significant drawdowns. However, not all backtesting is created equal. Basic backtests might only show return, but a comprehensive approach provides metrics like Sharpe Ratio, Sortino Ratio, maximum drawdown, and Calmar Ratio, all crucial for assessing risk-adjusted returns. The importance of reliable data for this process is underscored by Vector Solutions, which states that "effective risk management is done by considering information from the past and present as well as anticipating the future."

"Risk management can ensure appropriate levels of insurance to maximize financial success." – SentinelOne

Beyond historical backtesting, out-of-sample backtesting provides a more rigorous validation by testing strategies on data not used during their development, thus minimizing the risk of overfitting. Monte Carlo simulations further enhance this by generating thousands of hypothetical market scenarios, allowing traders to estimate the probability distribution of potential profits and losses. This statistical technique provides a clearer picture of extreme tail risks – events that are rare but have significant impact. Heatmaps can then visualize these risks, showing, for instance, how a strategy performs across different volatility regimes or asset correlations.

Another critical quantitative tool is Value at Risk (VaR), which estimates the maximum potential loss over a specified time horizon with a given confidence level (e.g., a 1% chance of losing more than $10,000 over the next day). While VaR has limitations, it provides a standardized metric for comparing risk across different strategies or portfolios. Stress testing complements VaR by simulating the impact of extreme but plausible market shocks, such as a "flash crash" scenario or a major geopolitical event, on a portfolio's value. These advanced analytical techniques allow traders to move beyond simple assumptions and gain a deep, data-driven understanding of their true risk exposure.

Continuous Monitoring and Adaptation in Algorithmic Risk Management

Risk management is not a static exercise; it's a dynamic, ongoing process that demands continuous monitoring and adaptation. Markets are constantly evolving, and a strategy that performed well last year might struggle today due to shifts in volatility, correlations, or underlying market structure. The IBM article on risk management emphasizes this, stating, "Risk management is a nonstop process that adapts and changes over time."

Real-time performance analytics are indispensable for this continuous process. Traders need dashboards that provide immediate insights into key metrics such as profit and loss, drawdown, exposure per asset, and current risk-adjusted returns. Monitoring for deviations from expected performance, unusual slippage, or unexpected correlations between assets can signal that a strategy's underlying assumptions may be breaking down. These early warnings allow for timely intervention before minor issues escalate into significant losses.

Furthermore, an effective risk management framework incorporates regular review cycles. This includes daily checks for unexpected market events, weekly reviews of strategy performance against benchmarks and risk limits, and monthly or quarterly deep-dives to assess the validity of core strategy hypotheses. If a strategy's performance deviates significantly or market conditions fundamentally change, the algorithmic parameters or even the strategy itself must be adapted. DNV notes that a structured approach involves "monitoring and review, and recording and reporting" as integral elements of risk management, which are further reinforced by certifications like ISO standards requiring regular audits and continual improvement.

The human element, while minimized in execution, remains critical in the oversight and adaptation phase. As Vector Solutions points out, "Risk managers must be aware of the human and culture factors that the risk management effort takes place in." This means traders must maintain a disciplined approach to reviewing their automated systems, not blindly trusting them. Identifying when to adjust risk parameters, pause a strategy, or even decommission it requires human judgment informed by robust data from continuous monitoring. This blend of automated execution and intelligent oversight is the hallmark of sophisticated algorithmic risk management.

How Horizon Addresses This

For serious traders who recognize the imperative of systematic risk management but lack the specialized coding skills or institutional resources, Horizon provides an advanced solution. Our AI-powered platform directly addresses the pain points of implementing robust risk controls in algorithmic trading.

- AI Strategy Generation with Integrated Risk: Horizon enables traders to generate custom trading strategies using AI, where risk parameters can be inherently considered during the strategy creation process, eliminating the need for complex manual coding of safeguards.

- Institutional-Grade Backtesting and Validation: Our platform offers an institutional-grade backtesting engine, complete with detailed performance metrics, out-of-sample backtesting, Monte Carlo simulations, and heatmaps. This allows traders to rigorously validate the robustness of their strategies under various market conditions and quantify potential drawdowns, adhering to the principles of comprehensive quantitative risk assessment.

- Automated Execution with Risk Controls: Once a strategy is refined, traders can connect their broker and deploy it for live trading with automated execution. This ensures that pre-defined risk management rules, such as stop-losses, position sizing, and maximum drawdown limits, are executed with precision and without emotional interference.

- Real-Time Monitoring and Adaptation: Horizon's real-time analytics provide continuous oversight of strategy performance, allowing traders to monitor key risk metrics and adapt their strategies as market conditions evolve, embodying the critical principle of continuous risk management.

- Strategy Marketplace for Learning and Refinement: The marketplace of community-built strategies offers insights into how others manage risk, providing a learning ground and a source for robust, community-vetted strategies that can be customized and further risk-managed on the platform.

Horizon empowers traders to transform their trading ideas into disciplined, systematically risk-managed algorithms, bridging the gap between sophisticated quantitative finance and accessible, no-code automation.

Conclusion

Risk management is not merely a component of trading; it is the bedrock upon which consistent profitability and long-term sustainability are built, especially in the era of high-frequency and algorithmic trading. From understanding core principles like systematic identification and analysis to implementing robust strategies through quantitative methods and maintaining vigilant, continuous monitoring, every step contributes to a more resilient trading operation. As markets become increasingly complex and interconnected, the ability to effectively manage risk becomes the distinguishing factor for serious traders. Leveraging advanced platforms like Horizon, traders can integrate institutional-grade risk management into their automated strategies, ensuring disciplined execution and robust portfolio protection. Explore Horizon's capabilities today and elevate your approach to risk-managed algorithmic trading.

Sources

- Risk management - Wikipedia

- Risk Management | US EPA

- 6 Principles of Risk Management | SentinelOne

- 8 Principles of Risk Management | Vector Solutions

- What Is Risk Management & Why Is It Important? | HBS Online

- What Is Risk Management? | IBM

- Risk Management Strategies: Methods & Techniques | DNV

- Seven risk management strategies for your business | MMA